The 2021 Municipal budget analysis began with a bit of welcome news: at the end of 2020 there was an operating surplus of almost $250,000. All departments contributed to this surplus through reduced costs stemming from temporary lay-offs, reduced hours of service, fewer events, reduced travel and office expenditures. Efforts to keep operating costs down continued in 2021 department operating budget requests, which were .7% lower than those in 2020. The library operates as a separate entity and did not experience reduced operating costs during 2020. It was an outlier in its request for a 9% increase in its operating budget as the Board continues to try to establish pay equity for its staff. The Building Department is funded by building activity and therefore does not impact municipal property tax bills.

Capital expenditures are funded by drawing from reserves, from specific grants and finally from the current year tax bill. In the second draft budget, $3,372,104 is directed to capital, however almost $2 million of this is headed into the Asset Replacement Reserves. For those familiar with financial statements, consider this as depreciation expense. The municipality has been increasing its contribution to this reserve in anticipation of the 2024 deadline when legislation requires municipalities to have an asset management plan for all municipal infrastructure assets that demonstrates an ability to maintain them. Another capital expense in this year’s levy is the final payment of $194,078 for the Millbrook Dam reconstruction. This amounts to 2% of the total property tax revenue for the municipality. While the expense falls off next year, the new Community Centre will be included in the municipal assets for which reserves are required.

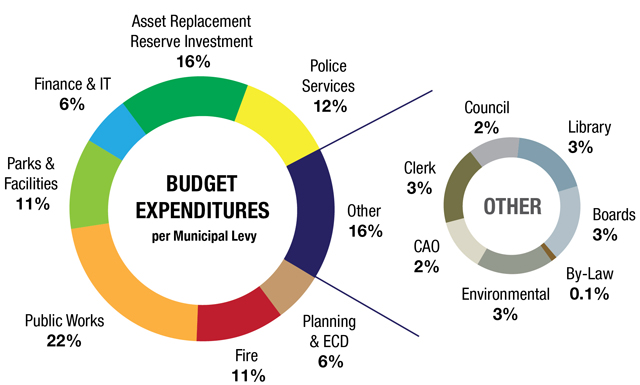

The pie chart below, courtesy Director of Finance Kimberley Pope, illustrates the distribution of this year’s tax payer dollars to each department and includes Council directives from the latest budget meeting.

Property tax bills will not reflect the impact of the municipal, county and educational rate changes until the final tax bills are distributed in July. By law, interim bills are a maximum of 50% of the previous tax year. This means the final invoices are higher so the municipality can catch up. The final budget approval is scheduled for February 16th. KG